Chris is an award-winning former journalist with 15 years of experience in the mortgage industry. A national expert in VA lending and author of “The Book on VA Loans,” Chris has been featured in The New York Times, the Wall Street Journal and more.

Updated on December 26, 2023 Veterans: Check your $0 down eligibility today! Expert Reviewed At a GlanceAs with any mortgage option, VA loans have pros and cons that you should be aware of before making a final decision. So let's take a closer look

VA loan pros and cons." />

VA loan pros and cons." />

VA loan pros and cons." />

VA loan pros and cons." />

VA loans are often one of the most attractive home financing options for Veterans and military borrowers - 2022 was another record-breaking year for the VA loan, with the VA guaranteeing more than 1 million VA loans. However, the VA loan isn't always the best financial choice for every borrower.

Here we dive into the pros and cons of the VA loan program and the most significant financial considerations to keep in mind when choosing your mortgage.

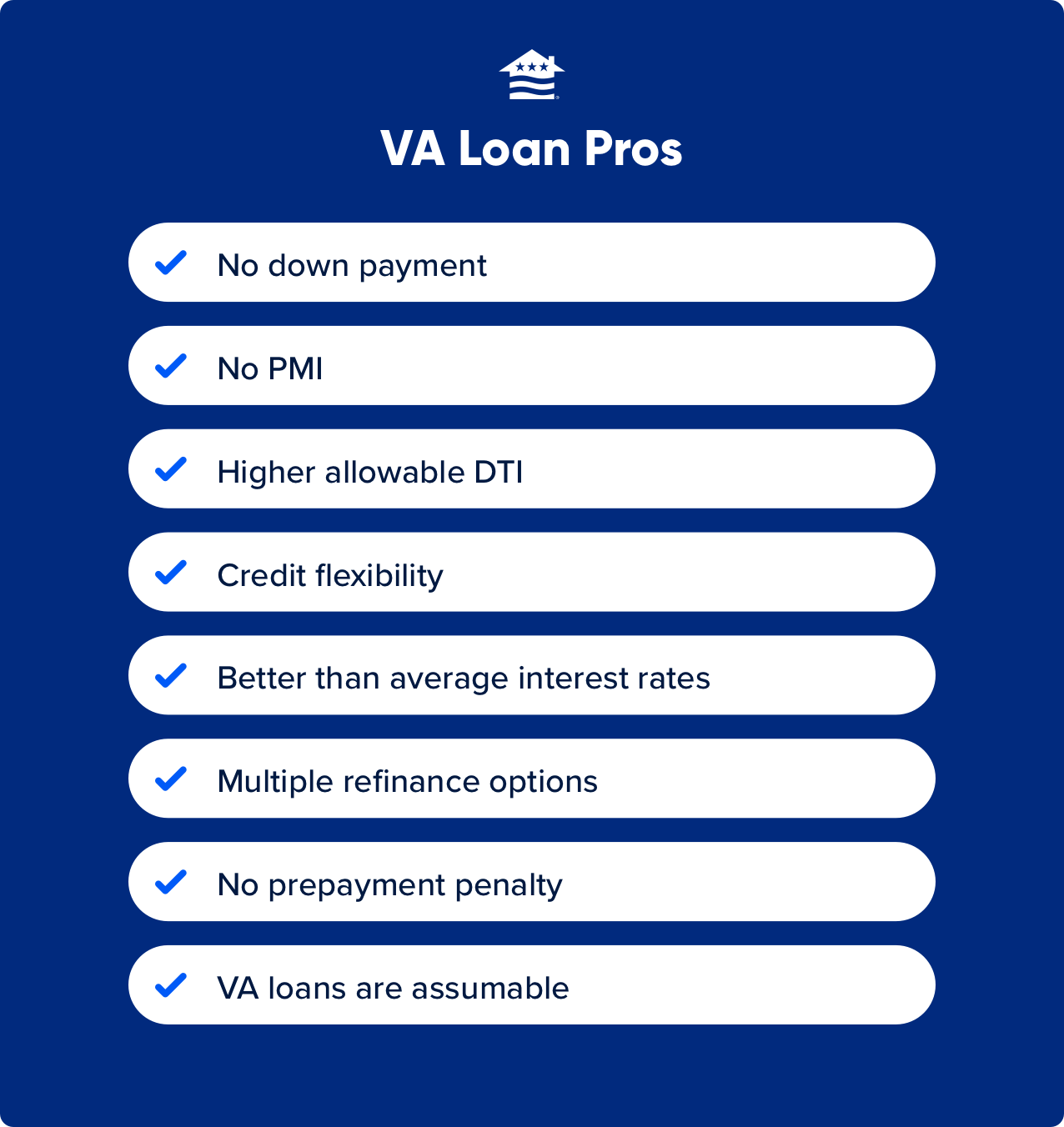

VA loan pros include no down payment, no PMI, higher allowable DTI, credit flexibility, better than average interest rates, multiple refinance options, no prepayment penalty, and assumable." />

VA loan pros include no down payment, no PMI, higher allowable DTI, credit flexibility, better than average interest rates, multiple refinance options, no prepayment penalty, and assumable." />

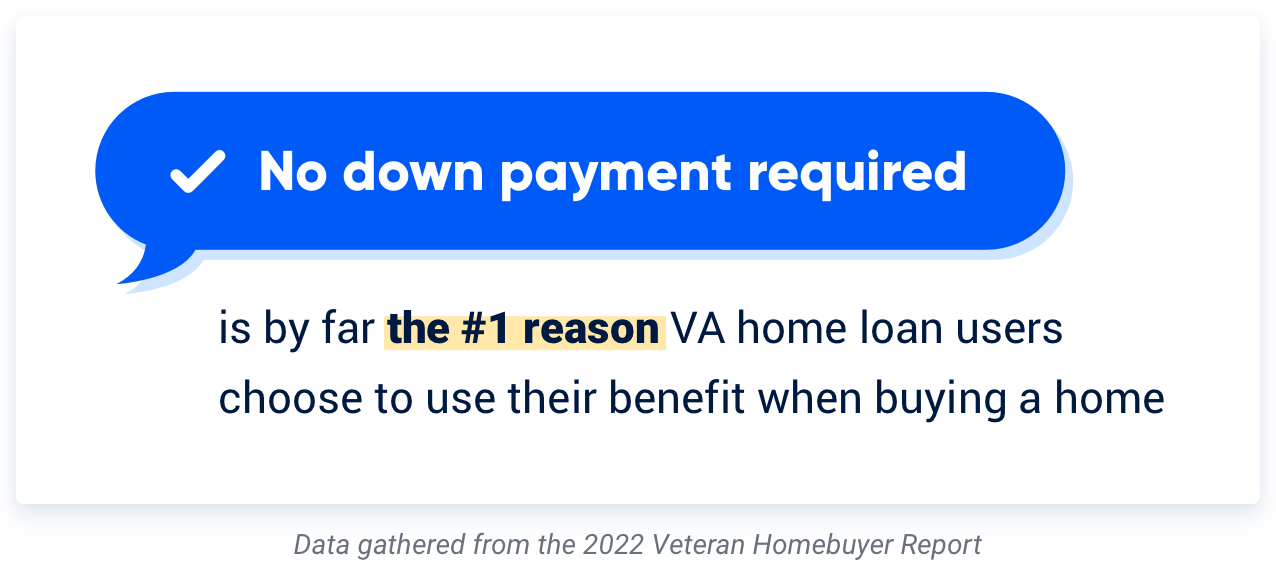

The ability to put $0 down is one of the biggest pros of VA loans. Qualified borrowers can borrow as much as a lender is willing to lend, all without needing a down payment.

FHA loans typically require a 3.5 percent minimum down payment, and for many conventional loans, it's a 5 percent minimum. On a $175,000 home purchase, that's a $6,125 down payment for FHA and $8,750 for conventional.

While this is a pro for many who can't afford a down payment, it could also be considered a con for some borrowers. It's possible to finance more than the home's value, which means you could start out with no equity in your home.

Private mortgage insurance, or PMI, is typically required for conventional borrowers who don’t have a 20% down payment at closing. No matter what you put down, VA loans do not have PMI, which can save Veterans thousands.

FHA borrowers have a form of PMI known as a Mortgage Insurance Premium (MIP) that typically spans the life of the loan. They also have an upfront fee due at closing.

Lenders will look at the ratio of your gross monthly income to your major monthly debts. The VA typically wants to see a debt-to-income ratio of 41 percent or less, but it’s possible to exceed that benchmark and still secure VA financing.

VA loans have no prepayment penalties. You can pay off your mortgage early or make additional payments without fear of being penalized financially.

Other loan products on the market, such as conventional and FHA, may have prepayment penalties, which can prevent borrowers from saving money.

The VA home loan program has a pair of refinance loans that can help qualified buyers lower their monthly payments or get cash back from their equity.

The largest benefit is to current VA borrowers who want to lower their rate through a VA Streamline refinance, also known as the VA Interest Rate Reduction Refinance Loan (IRRRL). IRRRLs allow Veterans to more easily lower their rate since you're refinancing from one VA product to another.

The VA Cash-Out refinance allows VA and non-VA homeowners to refinance and get cash at closing to pay down debt or take care of other needs. Keep in mind that refinancing may result in higher finance charges over the life of the loan.

See What You Qualify ForAnswer a few questions below to speak with a specialist about what your military service has earned you.

Some borrowers who qualify can be eligible for a VA home loan two years after a Chapter 7 bankruptcy, short sale, or foreclosure. The wait can be much longer for different loan types.

The VA also encourages lenders to offer foreclosure avoidance programs. The goal of VA loans isn’t only to get Veterans in homes but to keep them there.

Purchase contracts typically come with appraisal contingencies. The VA Amendment to Contract allows would-be buyers to walk away from a home if the VA appraisal comes back low.

In this scenario, the buyer would automatically receive their earnest money back and be free to walk away from the deal. Unlike other loan types, VA buyers cannot waive this appraisal contingency.

Assumptions have traditionally been a lesser-known and lesser-used pro of the VA home loan. The biggest benefit of assumptions is that borrowers can take over a Veteran’s loan and lock into interest rates lower than what is currently available. Looking into a VA loan assumption might be a huge win financially, especially once interest rates start to rise.

However, assumptions aren't for everyone. You can read more about assuming a VA loan here, but if another borrower assumes your VA loan, your entitlement may be wrapped up in that loan until the loan is refinanced or paid in full - unless the homebuyer assuming the VA loan is a Veteran and transfers their entitlement.

VA loans have had the lowest average fixed rate on the market for more than six years running, according to data from Ellie Mae. Housing data also show that VA loans typically feature lower closing costs and fees than conventional mortgages.

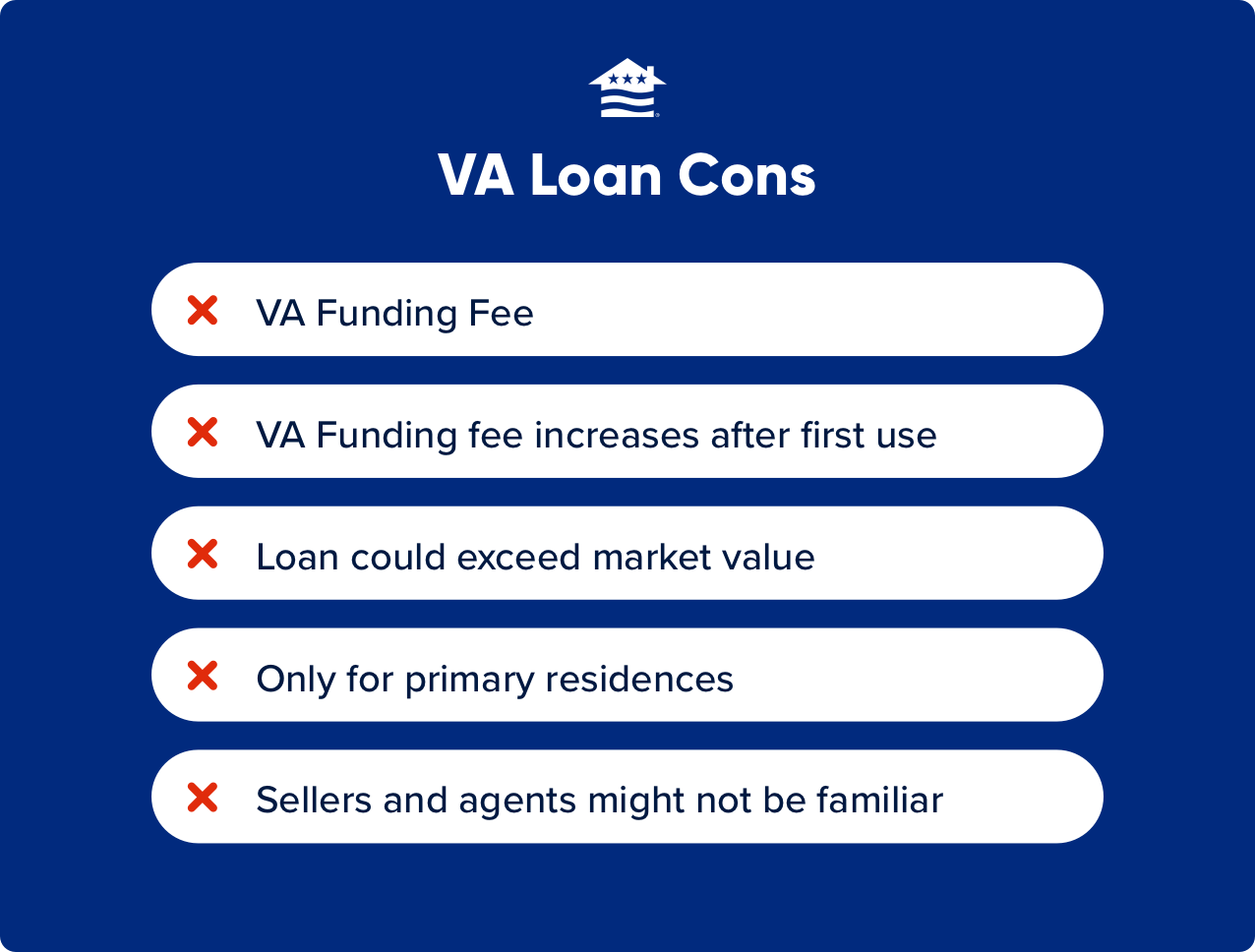

VA loans do come with some potential disadvantages. Let’s take a look at some of the larger potential cons of the program:

Most VA borrowers must pay the VA Funding Fee. The VA Funding Fee is a mandatory fee charged by the VA to help keep the program running for future generations.

The good news is you can finance this into the loan, and borrowers with service-connected disabilities, have a Purple Heart or are a surviving military spouse are exempt from paying the fee.

Veterans looking to reuse their VA loan benefit will find that the VA Funding Fee is higher than the first time. The first-time use fee is lower than the fee for all subsequent uses for most VA loans. Buyers can lower this fee if they make a down payment.

The VA loan isn't a loan program you can use to purchase a second home or an investment property. They’re intended for primary residences only, and the borrower must intend to live in it full-time. Because of this, there are occupancy requirements set by the VA. The only exception here is with the VA streamline refinance.

Working with a real estate agent familiar with the VA loan product is crucial to ensuring a smooth homebuying process.

Unfortunately, not every real estate agent is experienced with the program, which can result in wasted time if the property doesn’t meet the VA’s appraisal requirements or other guidelines.

Sellers may not be open to VA offers in a highly competitive housing market. It's not an extremely common occurrence but can happen when multiple offers are on the table.

This typically has much to do with the lack of understanding or myths and misconceptions surrounding VA loans.

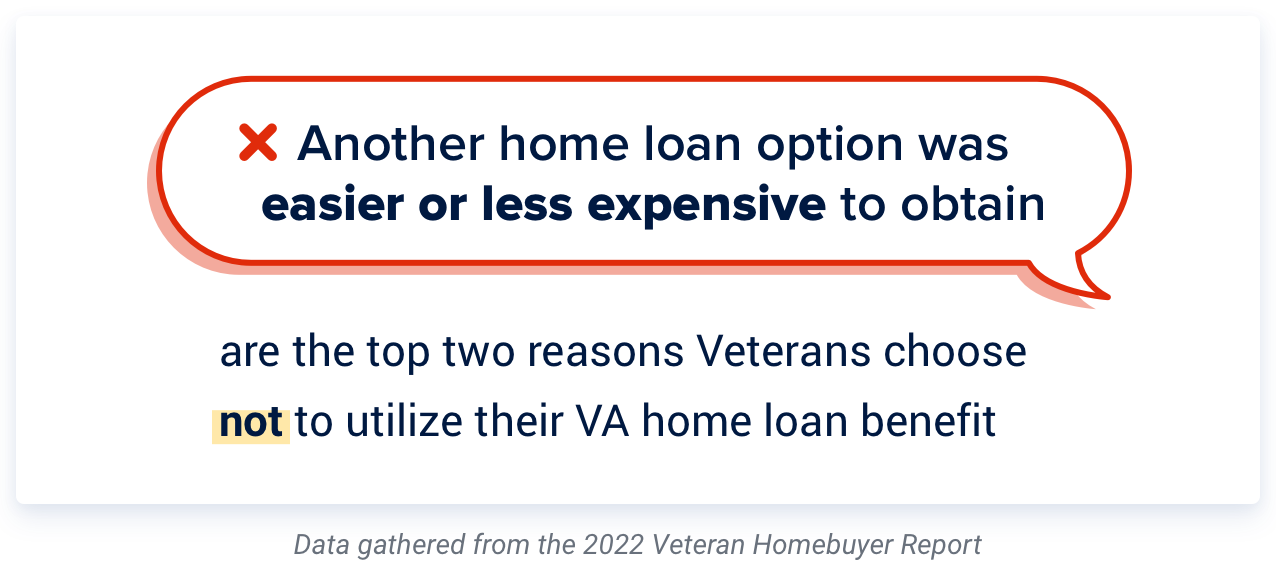

VA loans are typically the best option for VA homebuyers. However, it all depends on your unique financial situation.

If you're unsure of the best option for you, contact Veterans United. We can answer your questions about the VA loan and help you compare loan types to make the best financial decision.

See What You Qualify ForAnswer a few questions below to speak with a specialist about what your military service has earned you.

Chris Birk is the author of “The Book on VA Loans: An Essential Guide to Maximizing Your Home Loan Benefits.” An award-winning former journalist, Chris writes about mortgages and homebuying for a host of sites and publications. His analysis and articles have appeared at The New York Times, the Wall Street Journal, USA Today, ABC News, CBS News, Military.com and more. More than 300,000 people follow VA Loans Insider, his interactive VA loan community on Facebook.

About Our Editorial Process

Veterans United is recognized as the leading VA lender in the nation, unmatched in our specialization and expertise in VA loans. Our strict adherence to accuracy and the highest editorial standards guarantees our information is based on thoroughly vetted, unbiased research. Committed to excellence, we offer guidance to our nation's Veterans, ensuring their homebuying experience is informed, seamless and secured with integrity.

The VA funding fee is a governmental fee required for many VA borrowers. However, some Veterans are exempt, and the fee varies by VA loan usage and other factors. Here we explore the ins and outs of the VA funding fee, current charts, who's exempt and a handful of unique scenarios.

Can Your Mortgage Be Denied After Preapproval? Updated on April 15, 2024It is possible for you to get denied for a home loan after being preapproved. Find out why this may happen and what you can do to prevent it.