A cash flow statement is a critical tool for analyzing the current liquidity of any business venture. Cash Flow Projections are even more important as they help you understand not only your current liquidity, but also your probable cash flow position in the months and years to come.

All your budgets, investments, expenses, etc., will flow from your cash flow. This makes it compulsory for a business to invest in creating a cash flow projection that helps management understand the future cash position.

Some people believe that cash flow projections and profits are one and the same thing. But that is very far from the truth. Unless you deal only in cash and have no assets (like a freelancer, maybe), cash flow and profit and loss statement will have multiple divergences.

This is because all revenue segments and expenses considered while calculating the profits of the business might not necessarily be paid or received in cash. Profit and loss also considers non-cash items like depreciation and amortization. Profit and loss projections have a different purpose than cash flow projections, and serve a different finance functionality.

On this page, you will find our Cash Flow Projection Template, and two case studies that will help you to project the cash flows of your business over the future years.

But before we get to explaining the Cash Flow Projection Example, let’s define what a Cash Flow Statement is.

A cash flow statement is a summary of transactions representing inflows and outflows of cash over a period of time. A cash flow statement also breaks up the flow of cash into operating, financing, and investing activities for a more granular view.

Positive cash flow indicates a sound position for your company and demonstrates your ability to pay a robust return to its stakeholders.

The two main elements of the cash flow statement are inflows and outflows:

1- Inflows: Inflows represent the amount of cash received from the:

2- Outflows: Cash outflows represent the amount of money spent on:

Cash flow projection is a statement showcasing the expected amount of money to be received into, or paid out of, the business over a period of time. It is usually prepared on a monthly basis, but that can be reduced to a shorter period of say a week, and also can be extended to include 5 to 10 years.

Sometimes, a business looks profitable when looking at the profit and loss statement, but is actually facing financial problems in the form of cash shortages. Here, the cash flow statement will help you determine the company’s exact cash position, and detect any loopholes.

ABC Ltd reported a strong net profit of $2.20 million in the year 2019. But the company's cash flows were not bolstered by a similar amount. On closer inspection, the debt to revenue cycle is at 360 days as compared to the average 90 days seen by the industry. This can be a cause for concern as the company might be inflating sales, or its debtor repayment terms are so generous that it can cause a cash crunch in the near future.

The profit and loss statement will look like the following:

Depending upon the revenue circle, the company will receive only 0.55 million in cash from debtors which will affect its cash position. Putting the amount to be received from debtors in the cash flow projections template, balance will turn negative as reflected in the template below:

An electronics startup is expecting positive free cash flows of $24.92 million by year 5. But this calculation is based on a nominal market scenario basis. The same is represented in the template as follows:

If the cost of raw material (a critical key performance indicator - KPI) were to increase by 12%, the cash balance would reduce to just $4.24 million. This kind of dexterity in cash flow projections helps you manage and plan for different economic and operational scenarios.

The importance of cash flow projection is further enumerated below:

Read about "Importance of Cash Flow Forecasting" here.

Projected cash flows are an extension of preparing cash flow statements. There are two methods for preparation of cash flow statement, the direct and the indirect. Each of the methods considers changes in cash and cash equivalents from three activities: operating activities, investing activities, and financing activities.

To learn more about the three activities, click here.

Operating activities refers to the primary revenue-generation activities of a business. The nature of the business determines the actual classification of any transaction as an operating, investing, or financing activity.

There are two methods for arriving at cash flow from operating activities: the direct method, and the indirect method.

To see a detailed comparison of both the methods, click here.

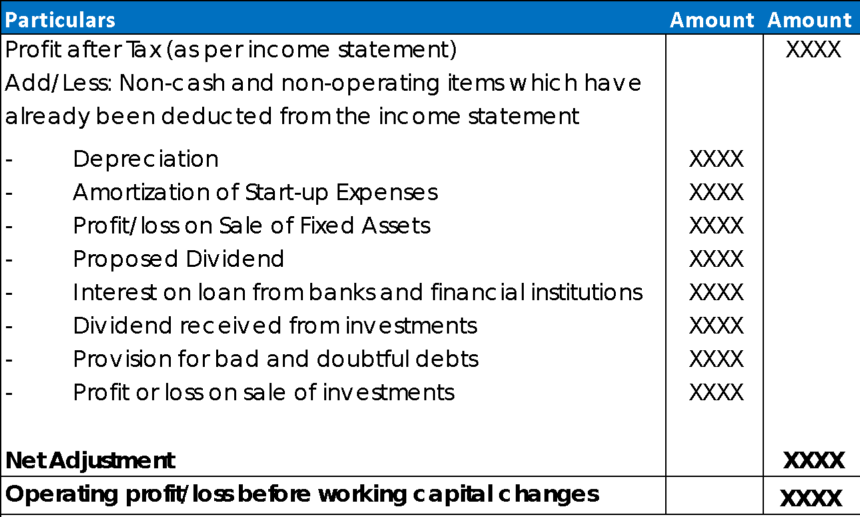

Under the direct method, each activity of revenue generation and expenses is recorded in the cash flow itself. On the other hand, under the indirect method, net profit or loss appearing in the profit and loss statement is adjusted for the non-cash expenses and working capital changes.

Under the direct method, cash flows from selling products or providing services is the starting point, where all the expenses paid in cash are deducted from the inflows recorded to arrive at the final figure.

The method makes it mandatory to construct the ledgers to arrive at the cash receipts or cash payments, and that is the reason that the indirect method is widely used in the market.

The sample cash flow from the direct method (taken from our template) is presented as follows:

Under the indirect method of cash flow projections, the net cash flow from operating activities is arrived at as follows:

After having adjusted the non-cash and non-operating activities, the adjustment for working capital changes would allow you to arrive at the exact amount realized or lost in operating activities.

The effect of working capital changes is to be adjusted in the following way:

Adjustment for Current Assets: Current assets represent inventory, accounts receivables, short term investments, prepaid expenses, etc.

This is perhaps best illustrated through an example. Suppose that during the previous month your accounts receivable stood at $5,000. At the end of the current month, the balance reaches $10,000. This would mean that additional $5,000 worth of debtors were not able to pay their dues, which will decrease the cash available within the company.

Adjustment for Current Liabilities: Current liabilities include accounts payable, taxes payable, interest payable, accrued expenses, bank overdrafts, etc.

In order to clearly understand the impact of changes in current liabilities, let’s assume that the balance sheet of the previous month contains accounts payable valued at $8,000. At the end of the current month, it’s at $2,000. This would mean that creditors have been paid an amount of $6,000 during the current month, which will ultimately reduce the cash balance available with the company.

The sample cash flow statement under the indirect method (taken from our template) is presented as follows:

To learn more about operating activities, Click Here.

Cash flow from investing activities is the result of changes in fixed assets: named land and buildings, plant and machinery, furniture, long term investments, etc. Some of the adjustments that are made while calculating cash flow from investing activities are:

The changes in the fixed assets are observed from the balance sheet. Heavy investment in fixed assets may result in an overall negative cash flow trend for the company. But that may not always have an adverse impact on a business, as it can be a part of the expansion strategy of the company.

To learn more about investing activities, Click Here.

Cash flow from financing activities records the transactions related to inflow of funds in the form of capital, investor funds or debts, and repayment of the same in the form of instalments, dividends, interest, buyback, etc. The details covered in this section are:

In order to find information with respect to the line items mentioned above, you can have a look at the debt and equity section of the balance sheet, along with a statement of retained earnings.

To learn more about financing activities, click here.

Once the cash flow statement construction is completed, the projections become an extension of the original process. You need to evaluate the following for estimating your cash flows for the upcoming months/years:

Accordingly, your cash flow projections for the coming years need to reflect the above scenarios in the cash flow projection model.

To learn even more about cash flow projections, click here.

To know more about the uses of cash flow projection, click here.

Considering the uses and advantages that are offered by the cash flow projections to different users, it can be concluded that it is one of the best measures used by investors to check the viability of any project or business venture.

Business decisions related to buyback of shares, repayment of the debt, business expansion, payment of dividend, merger or acquisition, capital investment and addition of new products to the portfolio of existing ones are all backed by this powerful projection model.

As a business owner/manager you need to invest the time and resources to ensure that cash flow projections become a compulsory planning tool for your organization's financial health.

How useful was this template?

Click on a star to rate it!

Average rating 4.5 / 5. Vote count: 10

No votes so far! Be the first to rate this template.

Help us improve!

How we can improve this template?